Think of landlord insurance as a purpose-built risk management tool for your portfolio. It's a specific policy designed to shield rental properties from the unique risks that come with having tenants—property damage, liability claims, and lost rental income. For any company managing hundreds or thousands of units, it's not just another line item on the P&L. It’s the financial foundation of a scalable and resilient operation.

Protecting Your Portfolio Is Protecting Your Revenue

When you’re overseeing a distributed portfolio, risk isn't just a possibility; it's a daily operational reality. A small kitchen fire in one unit, a slip-and-fall lawsuit, or a major storm can quickly spiral from a minor maintenance ticket into a serious financial drain that impacts your cost per door and net operating income (NOI).

This is where landlord insurance proves its worth. It’s built to handle the realities of tenant-occupied properties in a way a standard homeowner’s policy never could. It's easy to get them confused, but for a property management company, the difference is critical.

Key Differences From Homeowner's Insurance

One of the most common—and costly—mistakes a property owner can make is assuming their homeowner's policy is enough for a rental. The two policies are worlds apart.

Liability Focus: Landlord insurance is heavily focused on liability protection for incidents involving tenants and their guests. A standard homeowner's policy just doesn't account for this, leaving a massive gap in your coverage that could jeopardize the entire portfolio.

Property Coverage: It covers the landlord's personal property that’s used by the tenant, like refrigerators or washing machines. It does not cover the tenant's personal stuff—that's what renter's insurance is for.

Revenue Protection: This is the big one for portfolio managers. Landlord insurance includes loss of rental income coverage. If a unit becomes unlivable because of a fire or flood, this feature reimburses you for the lost rent. It’s a game-changer for maintaining steady cash flow and protecting your vacancy loss metrics, and it’s completely absent from homeowner's policies.

Getting these distinctions right is step one. For property managers, this isn't just about protecting buildings; it's about protecting the revenue streams your clients depend on. For landlords, knowing their investment is properly insured is non-negotiable. Viewing insurance as a strategic asset is key to running a secure and scalable operation.

Understanding Core Property Protection

At its heart, any good landlord insurance policy is about protecting the physical assets that generate your income. Think of it as the financial bedrock for your entire portfolio. Two key coverages make up this foundation—dwelling coverage and other structures coverage.

Dwelling coverage is exactly what it sounds like. It protects the main building where your tenants live, from the roof and walls down to the guts of the property like plumbing and electrical systems. Whether it's a single-family home or a 20-unit apartment building, this is the core protection for the structure itself.

Other structures coverage handles everything else on the property that isn't attached to the main building. We're talking about detached garages, fences, storage sheds, and even retaining walls. These might seem like small-ticket items, but when you manage hundreds of properties, the cost to replace them can add up fast.

Calculating Your Portfolio's True Replacement Cost

One of the most common—and most expensive—mistakes a landlord can make is insuring a property for its market value. Insurance isn’t about what you could sell it for; it’s about the replacement cost. This is the real-world price tag to rebuild that entire structure from scratch with today's labor and material costs. Getting this number right is a make-or-break task for property managers.

Let’s say a kitchen fire breaks out in one unit of a ten-plex. Your dwelling coverage is what pays to repair that unit and fix any smoke or water damage in the neighboring ones. If your coverage limit is too low, you're on the hook for the difference, which comes straight out of your net operating income (NOI).

Now, scale that up. Imagine a nasty windstorm rips through a neighborhood, damaging the roofs and fences of 50 of your single-family rentals in one afternoon. The only way to weather that kind of large-scale event without a massive financial hit is by having an accurate replacement cost calculated for every single property before disaster strikes.

Key Takeaway: You absolutely must conduct an annual review of the replacement cost value (RCV) for every property in your portfolio. Construction costs have shot up in recent years, and an outdated policy limit is a recipe for being dangerously underinsured.

Navigating Common Policy Exclusions

No insurance policy covers everything. Knowing what isn't covered is just as critical as knowing what is. This is where you build a truly comprehensive risk management strategy and avoid getting blindsided by unexpected costs.

Most standard landlord policies will not cover damage from:

- Floods: This is almost always a separate policy, typically purchased through the National Flood Insurance Program (NFIP) or a private insurer.

- Earthquakes: Just like floods, you'll need a special add-on (an endorsement) or a completely separate policy for earthquake damage.

- Sewer Backup: Damage from a backed-up sewer or drain is a common exclusion, but you can usually add this coverage back on with an endorsement.

- Neglect or Wear and Tear: Insurance is designed for sudden, accidental events—not problems that crop up because of deferred maintenance.

For anyone managing a portfolio, finding and plugging these gaps is non-negotiable. It all starts with diligent property inspections and rock-solid documentation. Keeping detailed records of a property’s condition is essential, as poor documentation can complicate any claim.

Being proactive is also key. For instance, burst pipes are one of the most frequent and costly claims, so understanding the common causes of burst pipes and prevention tips can save you a massive headache.

By accurately valuing your assets and thoughtfully closing any coverage gaps, you turn your insurance from a simple line-item expense into a powerful shield for your business. This foundational layer of protection is the first step to building a resilient and scalable operation.

Shielding Your Business From Liability Claims

While a broken pipe or a roof leak is a tangible, predictable risk, the biggest financial threat to your portfolio often comes from a single, unexpected incident. A slip on an icy walkway, a tenant's dog biting a guest, or a fall caused by a faulty railing can trigger a lawsuit that puts everything you’ve built at risk.

This is where liability protection becomes one of the most critical parts of your landlord insurance. Think of it as your financial shield. It’s designed to cover legal defense fees, settlements, and medical bills if a tenant or guest gets hurt on your property and you're found legally responsible. For property management companies overseeing hundreds or thousands of doors, that risk multiplies with every single unit.

The potential for massive claims is very real. The global landlord insurance market hit around $20.7 billion in 2023 and is expected to climb to $40.9 billion by 2032. This growth is partly fueled by a rising awareness of just how significant these liability risks can be. You can explore more data on this market growth to see why robust coverage is no longer just an option.

From Minor Incident To Major Lawsuit

Let’s play out a scenario that happens all the time. A tenant in one of your single-family homes reports a loose handrail on their back deck. Before your maintenance team can get there, the tenant hosts a barbecue. A guest leans on that exact railing, it gives way, and they suffer a serious back injury.

Suddenly, your company is on the hook for a lawsuit demanding compensation for:

- Medical Bills: Everything from the ER visit and surgery to months of physical therapy.

- Lost Wages: The injured person might not be able to work for a long time.

- Pain and Suffering: This is compensation for the physical and emotional distress caused by the injury.

- Legal Defense Costs: Attorney fees add up fast, even if you’re eventually found not at fault.

Without the right liability coverage, those costs come straight out of your pocket, draining your operational budget and hurting the profitability of your entire portfolio. A single claim can easily rocket past six figures, which is why this coverage is non-negotiable for any large-scale property management operation.

Why Standard Liability Limits Just Don't Cut It At Scale

Most landlord policies come with standard liability limits of $300,000 or $500,000 per incident. That sounds like a lot, but for a property management company with a large portfolio, it's often dangerously low. Jury awards for personal injury lawsuits have been climbing for years, and one serious incident could blow past those limits in a heartbeat.

Strategic Insight for Portfolio Managers: When your portfolio is worth millions, a standard liability limit is a massive blind spot. One judgment that exceeds your policy limit puts all of your business assets—and maybe even your clients' assets—on the line.

This is exactly why a commercial umbrella policy is so vital. An umbrella policy adds an extra layer of liability protection, kicking in only after your primary landlord policy's limits are completely used up. These policies are surprisingly affordable and can add $1 million, $5 million, or even $10 million in extra coverage.

For a company managing 1,000+ units, an umbrella policy isn't a luxury—it's a core part of a smart business strategy. It gives you the financial backstop to operate confidently, protecting your company from that one catastrophic claim that could otherwise derail your growth for years to come.

Protecting Your Revenue With Loss Of Income Coverage

For any property management company, a unit forced vacant by damage isn't just an empty space—it’s a hole punched directly in your gross potential rent. Dwelling coverage is great for rebuilding the walls, but it does nothing to answer the immediate question: what about the income that unit was supposed to be generating?

This is exactly where loss of income coverage (sometimes called fair rental value coverage) becomes absolutely essential. It’s designed for one specific job: to protect your revenue stream when a covered event, like a fire or a burst pipe, makes a unit uninhabitable. This coverage pays you for the lost rent you would have otherwise collected, turning a potential financial disaster into a manageable bump in the road.

What A Single Vacancy Can Really Cost You

The financial health of a large portfolio is built on predictable, consistent cash flow. Any unplanned vacancy throws a wrench in the works, hitting your net operating income (NOI) and your clients' bottom line.

Let's break it down with a simple scenario:

- Average Monthly Rent: $2,000 per unit

- The Incident: A kitchen fire takes one of your units offline.

- The Downtime: Repairs are projected to take three months.

Without loss of income coverage, that one fire just created a $6,000 revenue gap. Now, multiply that across a portfolio of hundreds or thousands of units. The financial bleeding escalates fast, impacting everything from your maintenance budgets to your quarterly performance reports.

The Bottom Line: Loss of income coverage transforms an unpredictable revenue gap into a predictable insurance claim. It allows you to maintain financial continuity, ensuring that a physical disruption doesn't derail your entire operational budget.

How The Coverage Works In The Real World

This isn't just a theoretical safety net; it's a practical tool that keeps your operations running smoothly. When a covered disaster strikes, the claims process for the lost rent is usually pretty straightforward.

Your policy will reimburse you for the "fair rental value" of the property for the time it's considered unlivable. This period typically lasts until the repairs are finished, allowing you to focus on getting the unit back on the market without the added stress of a gaping hole in your rent roll.

Most policies will keep this coverage going for a set period, often up to 12 months, which gives you a significant buffer for even the most extensive repairs. This is a lifesaver for managers of large or scattered portfolios where coordinating major renovations can be a serious logistical puzzle.

Making It A Core Part Of Your Risk Strategy

If you’re an operations director or portfolio manager, think of loss of income coverage as your KPI protector. Your vacancy loss metric is a critical sign of your portfolio’s health, and this coverage directly defends it against one of its most volatile threats.

When you’re reviewing your landlord insurance options, zero in on the limits for this feature. Some policies will cap the payout at a percentage of the dwelling coverage, while others offer more generous standalone limits. For a large-scale operation, making sure this coverage actually aligns with your potential revenue loss is one of the most important parts of your annual insurance review.

Ultimately, this coverage is the bridge that carries your revenue over the chaos caused by property damage. It’s a non-negotiable tool for maintaining financial predictability and protecting the profitability of your entire portfolio.

Tailoring Your Policy With Optional Coverages

The core parts of your landlord policy—dwelling protection and general liability—are the foundation. But let's be honest, they don't cover every weird, messy, or expensive reality of managing rental properties. For anyone overseeing a diverse portfolio, relying on a one-size-fits-all policy is a massive gamble.

This is where optional coverages, or what insiders call "endorsements," become your best friend. These add-ons are designed to plug the specific gaps that standard policies leave wide open, giving you a financial safety net for the real-world scenarios you actually face.

High-Value Endorsements For Large Portfolios

You could get lost in a sea of potential add-ons, but a few consistently deliver exceptional value for property managers who need to keep things efficient and financially sound. These are the ones that tackle the sneaky risks that can quietly blow up into major, unbudgeted headaches.

- Vandalism Coverage: This is a big one, especially for units sitting empty between tenants. Standard policies often won't cover vandalism if a property has been vacant for more than 30 or 60 days—a situation that's all too common during turnover. This endorsement makes sure you're covered for the broken windows, graffiti, and other malicious damage that can stall a lease-up and wreck your Days on Market (DOM).

- Ordinance or Law Coverage: This is probably the most overlooked but vital endorsement out there, particularly if you manage older buildings. Picture this: a fire damages 50% of an older property. Local building codes might force you to tear down the undamaged half and rebuild the whole thing to meet current standards. Your standard dwelling coverage only pays to fix the part that burned, leaving you with a jaw-dropping bill. This add-on covers the cost of demolition and those mandatory, expensive upgrades.

- Rent Guarantee Insurance: Don't mix this up with loss of income coverage. While loss of income helps when a fire or flood makes a unit unlivable, rent guarantee insurance protects you when a tenant simply stops paying. It kicks in during the eviction process, helping stabilize your cash flow when you need it most.

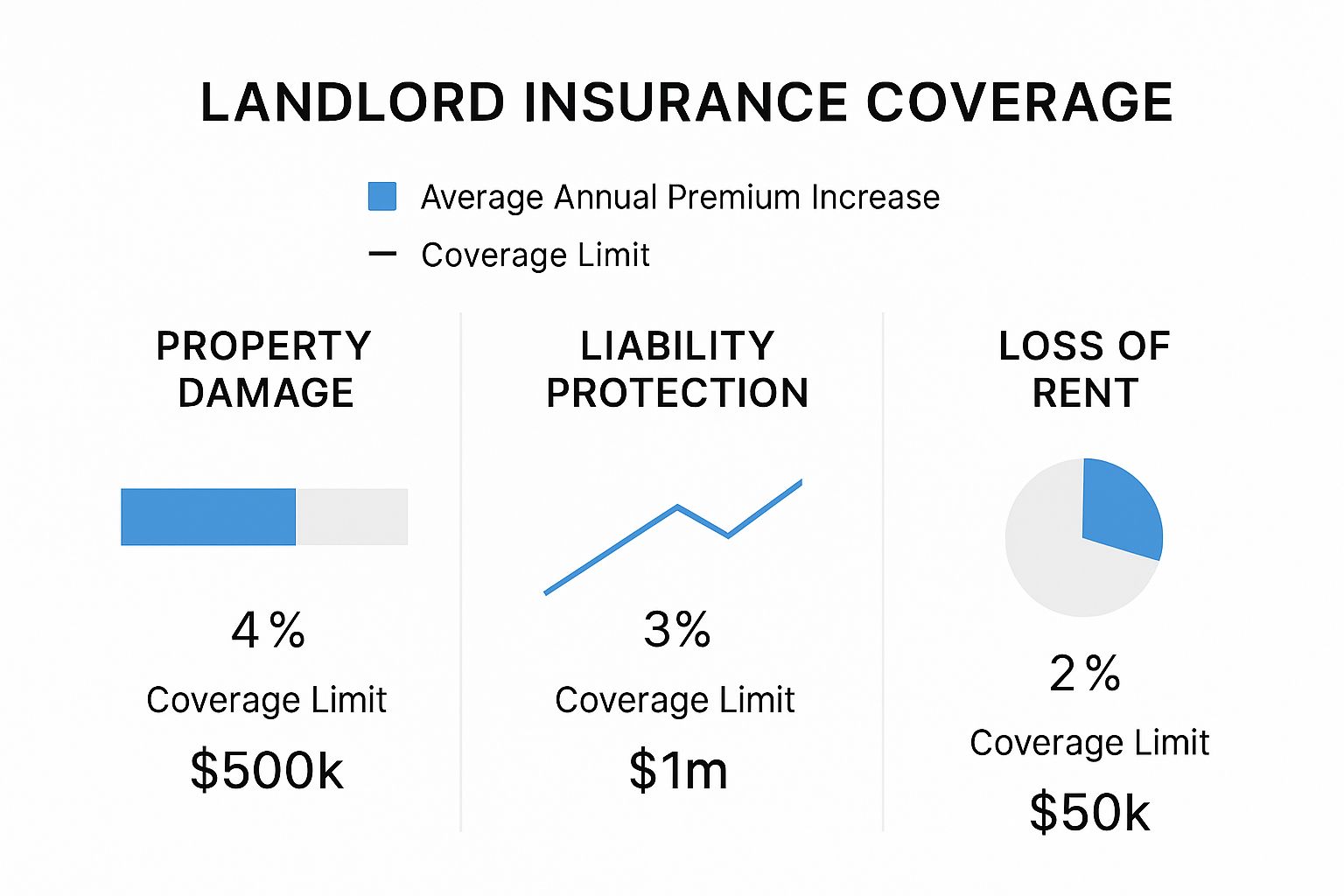

This visual breaks down how different coverage options can affect your premiums and protection levels.

It really highlights the trade-off between cost and coverage. You can see that while beefing up liability protection adds to the premium, those high limits are absolutely essential for shielding your business from a catastrophic lawsuit.

The Rising Cost And Complexity Of Coverage

Building the right policy means knowing what's happening in the insurance market right now. According to Forbes Advisor, landlord insurance premiums can range from 15% to 25% higher than standard homeowner’s policies, reflecting the increased liability associated with rental properties.

That increased cost is a key reason why a strategic approach is essential. Simply buying the most expensive policy isn't efficient; the goal is to allocate your insurance budget to cover the most probable and highest-impact risks your specific portfolio faces. You can dig into a full breakdown of these landlord insurance statistics to get a clearer picture for your own budgeting.

Strategic Takeaway: With insurance costs on the rise, a smart risk analysis is more critical than ever. Instead of paying for everything, you can strategically pick endorsements that match your portfolio's weak spots—like the age of your buildings or your average vacancy periods. This helps you build a cost-effective policy that puts maximum protection exactly where you need it.

Conducting A Portfolio-Specific Risk Analysis

The real key here is to stop thinking in generic checklists and start analyzing the unique DNA of your assets. You need to ask the tough questions to find your biggest vulnerabilities:

- What's the average age of my properties? The older your buildings, the more likely you'll be on the hook for expensive code upgrades after a claim. That makes Ordinance or Law coverage a must-have.

- How long do my units sit empty between tenants? If your average turnover time creeps past 30 days, Vandalism coverage for vacant properties becomes non-negotiable.

- Where are my properties located? If you have a cluster of properties in an area known for hail, floods, or sewer backups, getting specific endorsements for those events is just smart business.

By answering these questions, you can sit down with your insurance broker and build a policy that's a true financial shield, not just a piece of paper. It’s a proactive approach that ensures you’re ready for specific threats, not just vague possibilities.

How To Choose The Right Coverage Mix For Your Portfolio

Figuring out your insurance strategy isn't about ticking boxes on a generic policy. It's about building a financial shield that’s custom-fit to the real risks your portfolio faces. For an operations director or portfolio manager, this means going beyond a simple checklist and really auditing your assets.

This turns your annual insurance review from a dreaded line-item renewal into a powerful tool for protecting your portfolio's long-term health. It’s what makes your operations resilient and ready to scale.

Conducting A Strategic Portfolio Risk Audit

First, stop thinking of your portfolio as one big blob. Treat it as a collection of individual properties, each with its own unique risk profile. A systematic audit is the only way to find the gaps in your coverage and stop you from being over-insured in some areas while left dangerously exposed in others.

Your audit should get to the bottom of three core questions:

- Where are our properties concentrated? Do you have 200 units packed into a single flood-prone city, or are they spread across multiple states facing different risks like hail or tornadoes? A high concentration in one area might mean you need higher limits or specific disaster coverage.

- How old are our buildings? A portfolio full of older properties comes with the built-in risk of expensive, code-mandated upgrades after a fire or other major event. For these assets, Ordinance or Law coverage is an absolute must-have.

- Who are our tenants, and how often do they leave? High turnover often means longer vacancy periods. That makes vandalism coverage for vacant properties critical for protecting your units between leases.

Key Insight: A detailed risk audit transforms your relationship with your insurance broker. They go from being just a vendor to a strategic partner. You can pinpoint exactly where to invest in higher limits and where you can safely raise deductibles, making every premium dollar work harder for you.

Partnering With The Right Insurance Broker

When you’re managing properties at scale, you need a broker who gets the complexities of multi-unit portfolios. They need to speak the language of commercial umbrella policies, master policies for entire apartment complexes, and the niche endorsements that protect you from large-scale operational risks.

The landlord insurance market is getting bigger and more complicated all the time. In Europe, for example, the market is expected to hit nearly $27.77 billion by 2028, thanks to more rental investment and new regulations. You can discover more insights about this global market growth to get a feel for the trends affecting insurance costs and availability. A truly expert broker helps you navigate these shifts and lock in the best possible terms for your portfolio.

Your Top Landlord Insurance Questions, Answered

When you're managing a growing portfolio, the nuances of landlord insurance can get complicated fast. Let's clear up a few of the most common questions that come across our desks.

Does Landlord Insurance Cover My Tenant's Stuff?

That’s an easy one: no, it doesn't.

Think of it this way—your landlord insurance policy is there to protect your financial stake in the property. This means the structure itself, the roof, the walls, and any appliances or fixtures you own and leave in the unit. It's all about your assets.

A tenant's personal belongings—their couch, TV, laptop, and clothes—are entirely their responsibility. This is a critical distinction and exactly why requiring renters insurance is a non-negotiable best practice for savvy landlords. It closes that coverage gap and protects you from liability headaches down the road. You can dive deeper into these kinds of topics by checking out these top FAQs for landlords.

How Do Deductibles Work If I Own Hundreds of Units?

This is where things get interesting, especially for large portfolios. You can often structure your deductibles to work in your favor.

Instead of a per-unit deductible, you might opt for a per-building or per-occurrence deductible. Imagine a nasty hailstorm rolls through and damages the roofs on an entire neighborhood of your rentals. With a per-occurrence deductible, you pay that amount just once for the entire event, even if it affects 50 different properties. It's a much smarter, more cost-effective approach than paying 50 separate deductibles.

Do I Really Need Coverage for Vacant Properties?

Absolutely. A vacant property can feel like a sitting duck.

In fact, an empty unit is often at a higher risk for things like vandalism, break-ins, or a small leak that goes unnoticed and turns into a catastrophic flood. Most standard insurance policies include a vacancy clause, which can limit or even void your coverage if a property sits empty for more than 30 to 60 days.

The key is to keep your insurer in the loop. Always let them know when a unit becomes vacant so you can add a specific vacancy endorsement. It’s a small step that ensures your assets stay protected during tenant turnover.

And while you're thinking about protecting your buildings, don't forget other business assets. Getting smart about insuring items in storage is another piece of a truly comprehensive asset protection strategy.

At Showdigs, we get it. Minimizing risk and keeping vacancy days low are the cornerstones of a profitable portfolio. Our AI-backed leasing automation platform is built to get qualified tenants into your properties faster, protecting your revenue stream. See how Showdigs can slash your Days on Market by scheduling a demo at https://showdigs.com.